A seemingly innocuous measure buried in the budget held on 28 October raised an unexpected furore when Times of Malta flagged that the required years of social security contributions to qualify for a full pension will rise from 41 years to 42 for people born after 1976.

The measure quickly became the main topic of discussion on the night, with a public spat over whether or not this means that Malta’s retirement age is increasing.

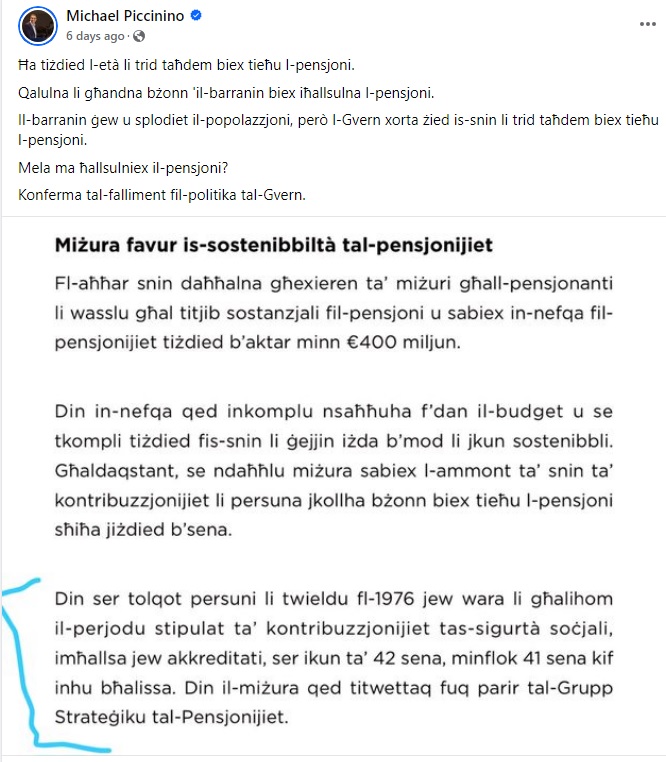

Several representatives from the Nationalist Party opposition posted a screenshot of measure’s description in the budget speech to their Facebook page, saying that the retirement age for Malta’s workers was increasing (although they carefully cropped out a paragraph in which the finance minister insists that this is not the case).

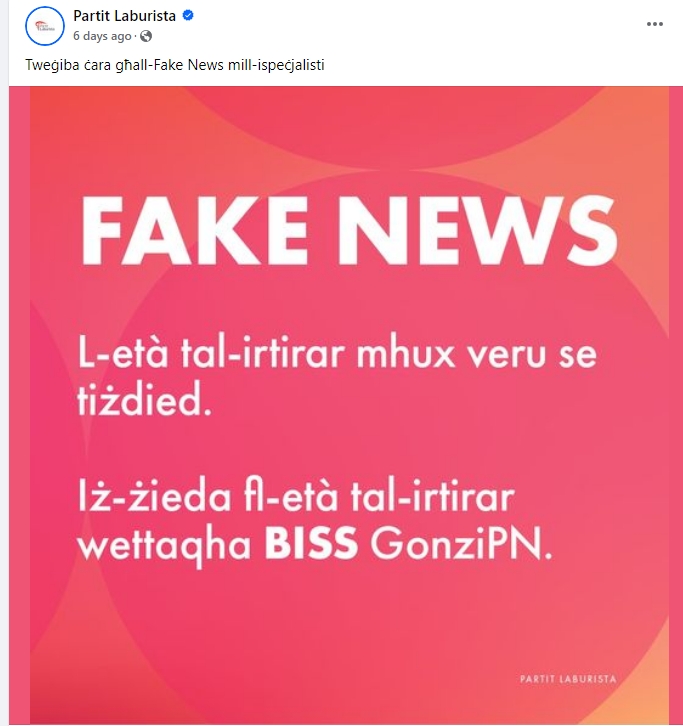

The Labour Party quickly retorted, branding the suggestion that the retirement age is increasing as “fake news”.

Robert Abela returned to the topic during a press conference held in the immediate aftermath of the budget speech, insisting that even if people started working relatively late because of their studies, they are entitled to social security credits that would safeguard their pension.

Caught between the bickering parties, a plethora of unsuspecting readers were left scratching their heads, wondering what this all means and whether they’ve been lumped with an extra year of work to look forward to.

So, what does the measure say?

In simple terms, if you were born in 1976 or later, you will now have to pay 42 years of social security contributions, rather than 41, as was previously the case.

This isn’t the first time that the number of contributions required has increased. The most recent increase, from 40 to 41 years, introduced in 2016, went largely unnoticed. Earlier still, the number of contributions had risen as part of the 2006 pension reform.

For some people, this most recent change won’t make the slightest bit of difference.

In practice, a person needs to have 42 years of contributions in the 47-year window between the ages of 18 and 65, meaning they can now afford to have up five years of unpaid contributions.

If you’ve started your working life by the age of 23 and keep working throughout your life, your 42 years of social security will take you right up to the retirement age of 65.

Even if you started working earlier than that, you would still have to wait for the statutory retirement age of 65 before you can claim your pension, even if you would have paid enough social security contributions well before your 65th birthday.

But things get a little more complicated if you start working later in life, or if you pause your working life, for whatever reason.

What happens then?

Let’s say you still find yourself studying well past your 24th birthday. You’ll quickly realise that there’s no way you’ll hit your 42 years of contributions before you turn 65, suggesting that you might have to work until you are 66 (or older) to qualify for a full pension.

The same might also be the case if you took time off your career for any number of reasons, whether it’s because you want to travel or to care for a loved one.

In any of these situations, you might need to work for 42 years to qualify for a full pension, rather than the previous 41.

But there are exceptions that cater for some of these scenarios.

Social security credits

In many (but not all) cases where people choose to enter the workforce late or pause their career, the government gives “social security contribution credits”.

These credits mean that even though you are not working, your social security contributions are still covered.

So, for instance, if you’re not working because you’re carrying out voluntary work (either in Malta or abroad), you are entitled to up to five years’ worth of credits.

If you’ve had to quit your job to care for your child, you’ll get up to four years in credits (or eight years if your child has a disability).

You will also receive credits in a whole range of other scenarios, such as if you are receiving unemployment or sickness benefit, or if you have been injured at work.

But you won’t receive any credits if you’ve taken time off to backpack your way across some far-flung corner of the world, unless you can convince the social security department that this was under the guise of voluntary work.

What about if I’m studying?

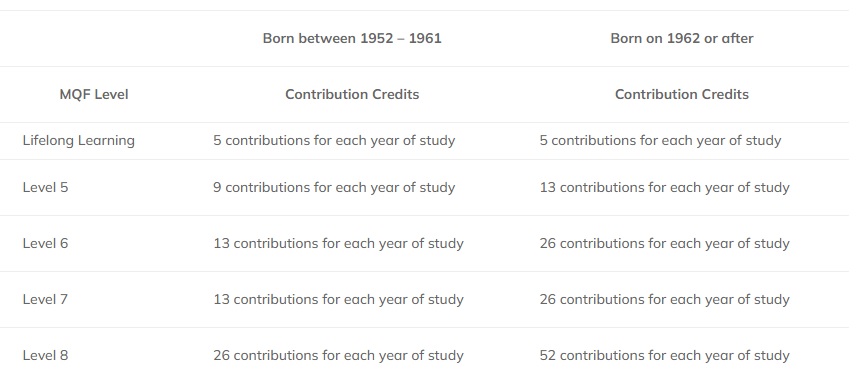

Students do receive credits throughout their studies, but just how many depends on the type of studies they are pursuing and when they were born.

If you’re studying at a doctoral level, and born after 1962, you’ll receive a full year’s worth of social security credits throughout the year, just as though you were working a full-time job.

If you’re studying at a level slightly below that (either for a Masters or Bachelor’s degree, or some sort of postgraduate diploma), you will receive half a year’s worth of credits for each year of your studies.

But students born between 1951 and 1962 receive half the amounts of credits listed above (because they need to pay fewer contributions to qualify for a pension in the first place), so they get half a year for doctoral studies and 13 weeks’ worth for graduate or postgraduate studies.

Do these credits apply retroactively?

Yes, those of us with greying beards will be relieved to find that our now-distant studies contribute to our approaching pension.

The same applies for those of us who have taken career breaks to care for children over the past years, or who have paused our working life for any of the reasons listed earlier.

So the retirement age isn’t increasing? Or is it?

Well, no, the retirement age isn’t increasing, at least not officially. And, ultimately, the measure will likely not really change much for many people.

But the measure may be bad news for people who have taken time off work for reasons that don’t qualify them for social security credits. In these cases, people may effectively have to work beyond their 65th birthday, until they’ve hit their 42 years of NI contributions, to receive a full pension.

But there are also ways to get around this.

If, upon turning 59, you realise that you have missing contributions, you can pay off up to five years’ worth of contributions to get you closer to the 42 years you need for a full pension, without having to work any extra years.

Verdict

The retirement age for Maltese workers hasn’t increased, but the number of contributions that a person must pay to qualify for a full pension has.

Many will not be impacted by the measure, either because they will have paid the full 42 years’ worth of contributions throughout their working life, or because they received social security credits while studying or during career breaks.

But for some people who started work late and do not qualify for social security credits, the measure may mean that they have to work beyond their 65th birthday if they want to receive a full pension.